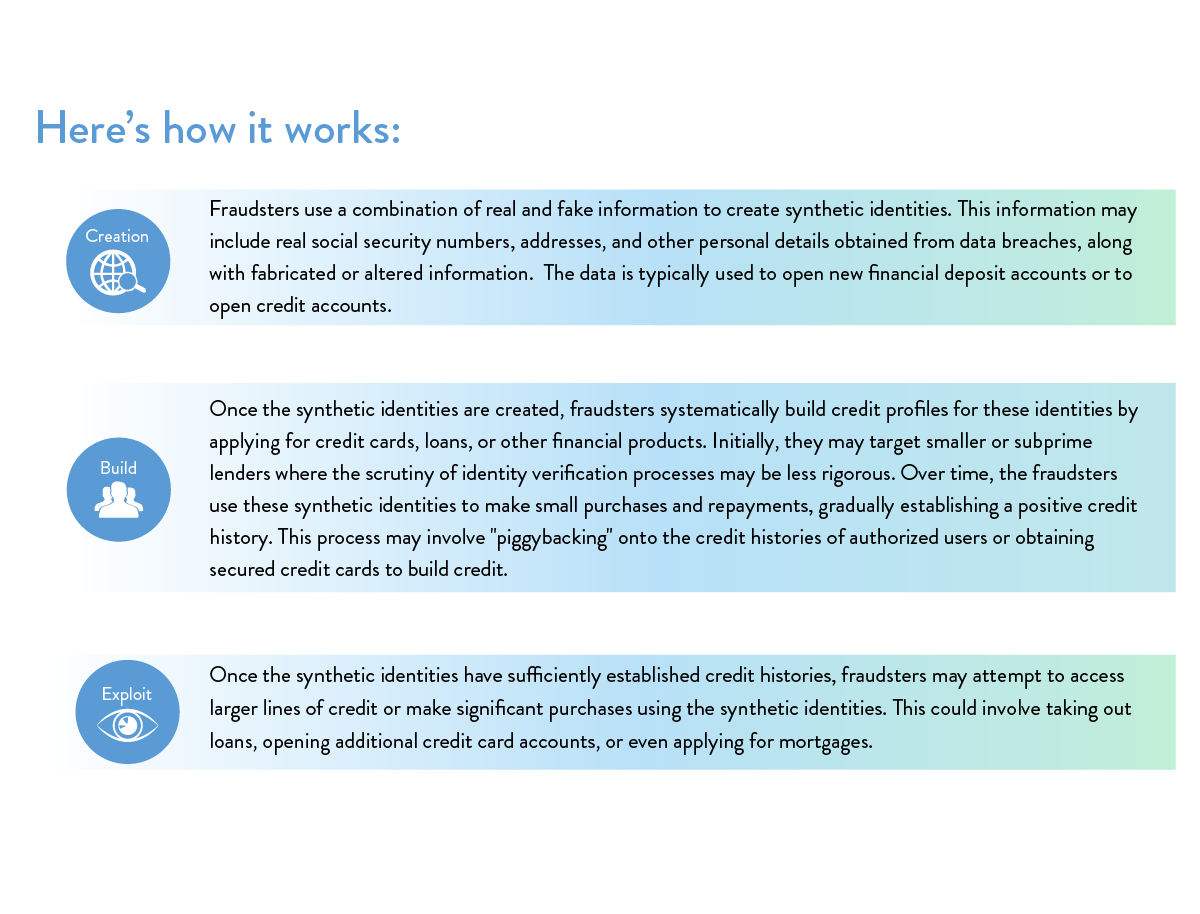

Synthetic identity fraud (SIF) is a type of fraud in which bad actors create fake identities using a combination of real and fabricated consumer information. Unlike traditional identity theft, where criminals steal and use the personal information of real individuals without their consent, synthetic identity fraud involves fabricating entirely new identities that may not correspond to any real person. Synthetic identity fraud aims for the bad actor to build a favorable credit profile for a fake person so the bad actor can take out a large amount of unsecured debt before riding into the sunset without making a single payment.

Synthetic identity fraud (SIF) is the use of a combination of personally identifiable information (PII) to fabricate a person or entity to commit a dishonest act for personal or financial gain.

Protection

Synthetic identity fraud can be challenging to detect and prevent because the identities being used are often completely fictitious. To combat synthetic identity fraud, financial institutions must adopt a more robust identity verification process and implement set of analytical tools to help them identify suspicious patterns and anomalies indicative of synthetic ID fraud, all of which start and end with data.

Credit unions need to partner with technology companies that can help them succeed. Implementing robust identity verification processes can help verify the authenticity of the information provided in credit applications is essential. This approach must involve cross-referencing application data with government-issued IDs, address verification services, and other sources to confirm the legitimacy of the applicant’s identity.

Additionally, the approach should examine relationships between different accounts, addresses, and social security numbers within a financial institution’s database to reveal connections indicative of synthetic identity fraud networks. This may involve analyzing shared addresses, phone numbers, or financial connections between seemingly unrelated accounts.

Finally, advanced document verification technologies should be used as a “stepped up” method to authenticate government-issued IDs and to correlate the applicant to the authenticated ID.

Ongoing monitoring

It is not enough for a credit union to simply implement defenses during the origination workflow. Credit unions should also implement systems and structures to continue to monitor their portfolio for synthetic fraud. By implementing robust monitoring systems, credit unions can detect irregularities in member profiles and flag potentially fraudulent activities before they escalate. Timely identification of synthetic fraud not only protects the credit union’s assets but also preserves the integrity of the financial system, fostering trust amongst its members. Moreover, proactive monitoring demonstrates the credit union’s commitment to security and ensures compliance with regulatory standards, ultimately contributing to the sustainability and resilience of the institution.

- Periodic Portfolio Scrubs – Synthetic identity fraud begins with a bad actor burrowing its way in as a member. From there, they build their credit profile and patiently wait for the perfect opportunity to exploit. One of the best defenses in the ongoing mitigation of synthetic identity fraud mitigation is to periodically scrub your member portfolio to find suspect identities before they can exploit an opportunity.

- Real-time Risk Monitoring – Credit unions should monitor high-risk activity online and respond to threats in real-time. This practice will mitigate all forms of fraud, including synthetic identity fraud. For example, many online banking platforms offer the convenience of self-service for various processes. If a member wants to update their email address, online banking is the first stop. Why not run the new email address against the members’ identity to verify the two pieces of data are correlated before making the update?

- Enhanced Login Defense – Most often, fraud is committed using digital services. To help identify fraud in real-time, Credit Unions should implement enhanced login defenses. This comes in many forms, but device screening is a perfect example. Examining a device at each login provides analytics about the device, the consumer’s network, device history, and much more to help stop fraud before it starts.

- Trend Analysis – Analyzing transaction patterns and account activity can reveal inconsistencies or unusual behavior that may indicate synthetic identity fraud. Sudden changes in spending habits, multiple applications for credit in a short period, or unusual account activity can be red flags. Utilizing advanced data analytics techniques, credit unions can analyze large volumes of data to identify patterns or anomalies associated with synthetic identity fraud. This may involve analyzing demographic information, credit history, and other relevant data points to detect inconsistencies.

- Collaborate – Being a part of a larger network of financial institutions that share information and collaborate is critical to mitigating all forms of fraud.

Conclusion

At the end of the day, the most crucial tool a credit union can have in its tool belt is partnerships. Partnering with innovative technologies and industry experts is paramount for mitigating fraud risks in the digital banking environment. By leveraging advanced analytics, machine learning algorithms, and cutting-edge fraud detection solutions, financial institutions can proactively identify and respond to emerging threats, such as synthetic identity fraud, account takeovers, and other threats persistent in the banking domain. Collaborating with industry experts allows credit unions to stay ahead of the fraud, benefit from best practices, and access specialized knowledge and resources. These partnerships enable banks to enhance their fraud detection capabilities, improve customer trust, and safeguard sensitive financial information in an increasingly complex and interconnected digital landscape.

To learn more about how eCU Technology’s partnership with Socure can help, click here to schedule a call.

REFERENCE for definition above